If you are working as an accountant in India, it is super obvious that if you can do US accounting work, you can get paid more and get better jobs.

Table of Contents

So why can’t people who know Tally start using QuickBooks or Xero and start earning in dollars already?

Most Indians with a background in accounting or bookkeeping are unable to tap into US clients because of one mental handicap – that they don’t know US GAAP.

Even those who have pursued MBA degrees, CA or CMA programs didn’t learn about it.

Let me tell you, learning about US GAAP is not hard at all.

Even if you are a B.Com student, you can do it.

In less than 25 mins (that’s what it will take to read this mail 3-4 times over), we will teach you at least 5 key US GAAP principles for common bookkeeping and accounting transactions, right now, in this email itself.

You can decide after that.

I will also compare this with Indian practices.

Our normal accounting on Tally, which most accountants and bookkeepers perform, is as per Indian GAAP.

Listed companies (and certain other large companies) follow a different standard called IndAS, which has quite a few similarities with IFRS in Europe.

US GAAP vs IndAS: 7 Key Accounting Differences

Let us see how to account for US GAAP for the 7 key items.

We will compare US GAAP with IndAS here.

Let us start with how the financial statements are to be presented first.

#1 – Presentation of Profit and Loss Account / Income Statement & Statement of Cash Flows

I’ll start with an easy one first.

The differences in the profit and loss account and statement of cash flows here are largely cosmetic.

- Under US GAAP, the income statement (i.e. profit & loss account) and statement of cash flows have to be presented for 3 years so that stakeholders have a comparative view.

- Under IndAS (applicable to large Indian corporations), it is to be presented for 2 years.

#2 – Treatment of Lease

How do you account for a simple office lease?

- Under IndAS, lease expense (rental) is treated as an expense in the year in which it is incurred. Plain and simple.

- US GAAP categorises leases differently. In a US financial statement, a typical lease is called an “operating lease”.

In addition to recognising the expense in the year that it is incurred under the profit and loss account, there is one more step that is to be taken.

- If the lease is over 12 months and has “material value” from the perspective of the company’s business, it will be classified as a “right of use” asset under the balance sheet.

- This is clubbed under plant, property and equipment, where such leases may be referred to as ROU assets.

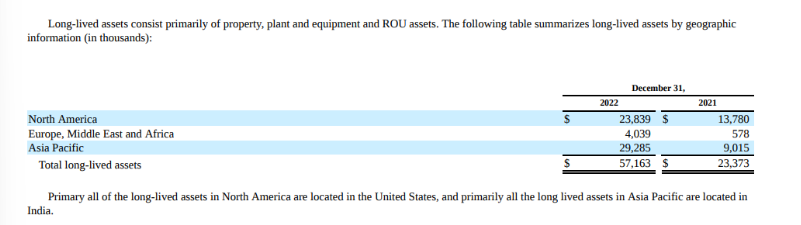

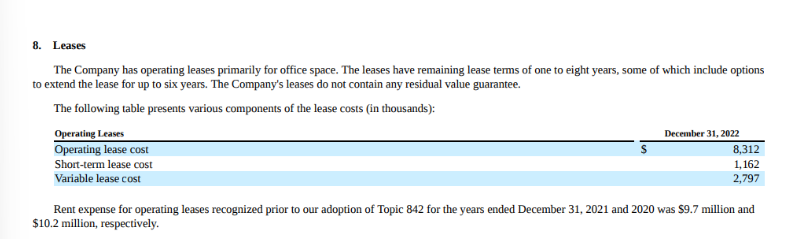

Here is how it is shown – we will see the Freshworks latest 10K statement (i.e. annual statement) filed with the SEC here:

The value of the future payments that must be made is also accounted for.

How do you account for the present value of a future payment?

- Typically, a discount rate is used, which must be disclosed in the financial statements.

#3 – Treatment of Inventory

Inventory treatment is mostly for manufacturing businesses, processing and assembling industry.

Those who are using Tally software in India for such businesses are already comfortable with it.

If you are not, you can learn.

- Under US GAAP, inventory is valued as per the LIFO method (i.e. last in, first out).

This can feel like a little bit of a juggle to figure out.

Why is the choice of costing method important?

Let me give an example. Imagine that I am an iPhone retailer.

- I have 10 iPhones of Rs. 1 lakh, which I purchased earlier and 10 iPhones, which I purchased later at 1.5 lakhs each, when the price had increased in the global market.

- The total cost of these 20 phones inventory is 25 lakhs.

- The first 10 and the next 10 iPhones had a different cost.

When I sell an iPhone, or if I have unsold inventory, what cost should I value on my books?

- Should I take the average into account? (The average cost of an iPhone is 1.25 lakhs.)

It will be too impractical to map the cost based on the serial number of the iPhone. Hence, US GAAP sets a uniform principle for it.

Let’s assume that at the end of the year, I have 10 unsold iPhones.

- Should I value them at 1 lakh, 1.25 or 1.5 lakh each as per my books?

- Under IndAS and IFRS, I cannot use LIFO; I must use FIFO (first-in-first-out) or weighted average cost.

- As per the FIFO principle, I must assume that the first 10 iPhones got sold, and the unsold ones are the ones I bought last, i.e. at 1.5 lakhs.

That means I can use 1.5 lakhs or 1.25 lakhs as the value.

Most businesses use a weighted average method.

- Under US GAAP, you can ALSO use LIFO, apart from the above methods, based on the accounting policy of the company.

That means you can assume that the more expensive iPhones were sold first.

What does this mean for US businesses?

- Businesses have more freedom to choose the inventory costing method, subject to disclosure.

- There will be restrictions on changing the accounting policy, as that will prevent comparison of results across years.

How does this affect financials?

- It impacts:

- Value of unsold inventory

- Cost of goods sold

- Profit

#4 – Valuation of Fixed Assets (Including Intangibles)

This is another interesting one.

Let’s assume that Walmart purchased a warehouse from Apple in the US for 10 million dollars.

This warehouse is in a prime location and is currently valued at USD 25m. However, the warehouse is not sold.

- How should the fixed asset be shown? Should it be shown at 25m or 10m?

- Under US GAAP, it must be shown at historical cost, i.e. at 10m dollars.

However, under IndAS or IFRS, you have to revalue the asset at 25m.

What if the value of the warehouse had fallen to USD 8 million?

- Same answer — in the US, you will continue to show it at historical cost, but under IndAS, it will have to be revalued.

How are these gains or losses shown?

- Under IFRS and IndAS:

- Gain → Other Comprehensive Income

- Loss → P&L as a non-operating expense

These are recorded as non-operating items because they arise from non-core activities.

#5 – Contingent Liabilities

How are commercial transactions, such as guarantees, accounted for?

How do you account for the risk of a liability if the court requires your client to pay damages to a third party?

These are contingent liabilities.

Let us say there is:

- A guarantee provided by your company

- A legal proceeding

- A tax notice

Which could potentially result in a liability of 5m dollars.

Under accounting standards, management must exercise judgment.

- Under US GAAP, if there is a high likelihood (over 75%), a provision needs to be made.

- Under IFRS, a provision is required if likelihood is 50% or more.

- Under IndAS, provisioning is not required unless legal confirmation and documentation exist.

#6 – Product Development Cost

How should research and development expenses be treated?

Tech companies invest heavily in building products.

- An app developed in 1 year could be used for several years.

Can a US company spread this cost?

- Under US GAAP, the entire product development cost must be expensed in the same year.

Exception:

- Software development cost can be capitalised and amortised.

- Under IndAS, development costs can be capitalised, but research costs cannot.

#7 – Revenue Recognition

- Under US GAAP, revenue is to be recognised when the product is sold or services are provided, as that is when you have the right to earn an income. It follows a 5-step model.

- IFRS and IndAS are the same.

- However, Indian GAAP, applicable to most private companies, does not follow this – they rely on the certainty of realising the income.

- If there is a doubt about whether payment will be received from the other side, revenue may not be recognised.

- In India, many clients do not pay, or pay on time, even if there is a contractual right to earn, so there is scope to not recognise revenue if payment is uncertain.

- US GAAP does not allow this.

How did you find this?

Watch this video to understand the differences between US GAAP and Indian Accounting Standards:

https://www.youtube.com/watch?v=bhXv0jCG8yI&feature=youtu.be

Do you think that with some preparation and practice, you could get better at it?

This is just the starting point.

What It Takes to Work on US GAAP

You should know how to do such work with respect to 20-30 items to be able to do this work for a US startup or SME.

Once you learn how to do this, it is possible to present/recast financial statements as per US GAAP very easily.

And then you can learn how to use bookkeeping and accounting software like QuickBooks.

It is possible to learn this in under 3 months.

How the Industry is Currently Working

The Big Four accounting firms, and a handful of Indian accountants who discovered this opportunity, are already doing this – they hire accountants in India, train them on a few important tasks in 1.5 months and then do global work from India.

The problem is that while they earn very well for this work, the Indian accountant or bookkeeper who works for them gets paid only 30-50K per month.

Also, they are working only for the top 5% of the large corporations.

95% of the businesses there are startups, SMEs and CPAs who run smaller practices, who cannot offshore such work to the Big Four.

Opportunity for Indian Accountants

If you can learn how to do this work and how to find and pitch to US clients, you can directly work with US clients and earn 3x-5x than in Indian jobs.

The market is very big and untapped; you have a massive cost advantage if you learn how to do the work, and there is very little competition as compared to Indian jobs.

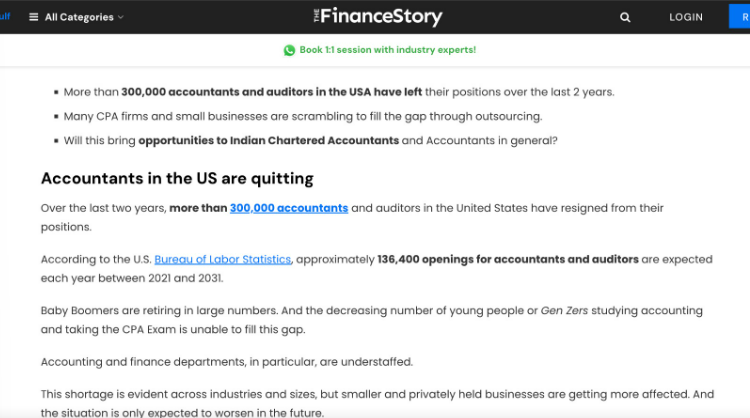

US Accounting Talent Shortage

The US is going to face a talent shortage as well:

Allow notifications

Allow notifications