A founder sits across a boardroom table and signs a term sheet to sell her mid-market software company. The number on the page is the one she spent two years dreaming about. She shakes hands, someone opens a bottle, and she goes home thinking the deal is done. It isn’t.

What she signed is page one of the M&A deal process, and roughly ninety days of hard work sit between that signature and the moment money moves. Within a week, a diligence team lands in her data room. Within a month, lawyers are drafting a definitive agreement clause by clause. And somewhere in a regulator’s office, a clock she didn’t know existed has already started ticking.

Here’s the thing most people learn the hard way about mergers and acquisitions. The term sheet feels like the finish line because it settles the price, but price is only one variable in a transaction with dozens of moving parts. Between signing that first document and closing the deal, a buyer has to verify every claim the seller made, both sides have to translate a one-page summary into a hundred-page contract, banks have to release financing, and antitrust authorities have to give the combination their blessing. Skip a step or get one wrong, and a deal that looked certain can collapse in week ten.

That gap between “we agreed on a price” and “the ownership has legally transferred” is where careers are made in corporate law and investment banking. It’s also where founders and sellers lose leverage they didn’t know they had. A junior M&A lawyer in Mumbai, a transaction-services analyst in Bengaluru, or a first-time seller in Pune all need the same thing: a clear map of what happens between term sheet and closing, in what order, and why the sequence can’t be rearranged.

The map is more universal than most people assume. Whether the target is a Delaware corporation or a private limited company in Gurugram, the deal moves through broadly the same stages, in broadly the same order. What changes across borders is the regulatory overlay: which competition authority has to clear it, which securities rules bite, and how ownership legally passes. Master the sequence once and you can read almost any deal, then layer the jurisdiction-specific rules on top.

That’s the promise of understanding this process properly. A person who can explain, without notes, how a deal moves from an initial approach through diligence and a signed share purchase agreement to a regulator-cleared closing is someone a deal team wants in the room. It’s the difference between memorising a list of stages and genuinely understanding why each one exists and what breaks if you skip it.

So this guide walks through the entire sequence. The three phases every deal moves through, all twelve stages from strategy to integration, the difference between a term sheet and a letter of intent, what due diligence really involves, the clauses that make or break a definitive agreement, why signing and closing are separate events, and the India-specific layer of CCI, NCLT, SEBI, and FEMA that turns a textbook deal into a live one. Let’s start with the shape of the whole thing.

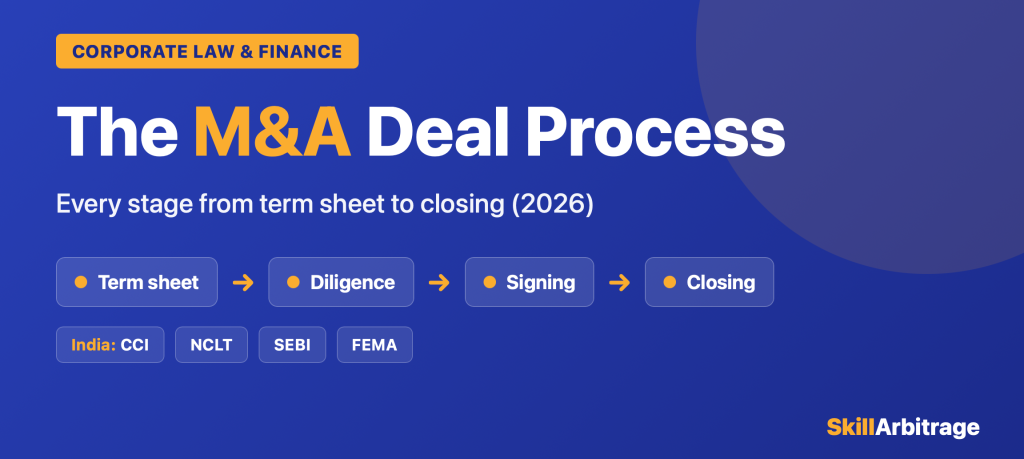

The M&A deal process moves through roughly 12 stages grouped in three phases: pre-deal (strategy, target sourcing, NDA, valuation), deal execution (term sheet/LOI, due diligence, definitive agreement, financing, signing), and completion (regulatory approvals, closing, post-merger integration). The term sheet opens the deal; closing transfers ownership once every condition precedent is satisfied.

The sections below move from the big-picture shape of the process to each individual stage, then into the negotiation documents, the signing-to-closing gap, the Indian regulatory layer, realistic timelines, and the mistakes that sink deals. Use the table of contents to jump to whatever you need first.

What the M&A deal process is, and the three phases every deal moves through

Why does the order matter so much? Because each stage produces something the next stage depends on, and skipping a gate almost always costs more than the time it saves. You can’t price a company you haven’t valued, you can’t value one you haven’t looked inside, and you can’t look inside without a signed confidentiality agreement first. The sequence isn’t bureaucracy. It’s risk management, translated into a workflow.

The M&A deal process defined: pre-deal to execution to completion

The M&A deal process is the structured sequence a buyer and seller follow to move a business from “we might do a deal” to “ownership has legally changed hands.” It groups into three phases. Pre-deal covers strategy, finding or preparing the target, signing an NDA, and a first-pass valuation. Deal execution covers the term sheet or letter of intent, due diligence, the definitive agreement, financing, and signing. Completion covers regulatory approvals, closing, and post-merger integration.

Most practitioners count around twelve distinct stages across those three phases, though the exact number depends on how you slice it. A simple private deal might compress several stages into a single afternoon. A cross-border acquisition of a listed company can stretch each one into months of its own. What stays constant is the shape: you narrow from a broad strategic idea to a specific target, verify that target exhaustively, paper the agreement, clear it with regulators, then close and integrate.

Think of it this way. The term sheet is the front bookend of the deal, and closing is the back bookend. Everything between them: diligence, drafting, financing, approvals, is the work that turns an agreed headline price into a legally binding, regulator-cleared transfer of ownership. Understanding that framing keeps you oriented no matter how complex a specific deal gets, and it’s the mental model the bankers who advise on these transactions carry into every mandate.

Why the sequence matters: the cost of skipping a gate

What experienced dealmakers know is that the stages exist to surface bad news early, while it’s still cheap to walk away. Due diligence sits before the definitive agreement for exactly this reason: you want to find the undisclosed lawsuit or the overstated revenue before you’ve signed a binding contract to buy, not after. A buyer who rushes diligence to close faster is trading a few weeks of speed for the risk of inheriting a problem worth far more than the deal itself.

A question that comes up constantly in corporate-law and finance forums is whether the stages can run in parallel to save time. Some can. Financing arrangements and diligence often overlap, and lawyers frequently start drafting the definitive agreement while diligence is still running. But the hard dependencies hold: you cannot sign a definitive agreement that reflects diligence findings before those findings exist, and you cannot close before regulators clear the deal. The art is compressing what can overlap without collapsing a gate that shouldn’t move.

How the modern staged deal process emerged

The disciplined, document-heavy process familiar today wasn’t always the norm. Through the merger waves of the late nineteenth and early twentieth centuries, deals were often struck on handshakes and light paperwork, with formal antitrust review largely arriving later as competition law matured. The leveraged-buyout boom of the 1980s, the mega-mergers of the late 1990s, and each subsequent cycle pushed diligence and contractual protection to become far more rigorous. Modern virtual data rooms, standardised share purchase agreements, and mandatory merger-control filings are the accumulated scar tissue of decades of deals that went wrong when someone skipped a step, which makes the process you’re learning, in effect, a checklist written in the aftermath of other people’s mistakes.

Phase 1: pre-deal strategy, sourcing, NDA and preliminary valuation

So what happens before anyone signs anything? A surprising amount of work, it turns out. This is the pre-deal phase, and it’s where a vague ambition (“we should acquire something in this space”) turns into a specific, priced opportunity. Get this phase right and the rest of the deal has a solid foundation. Get it wrong and you’re negotiating hard over a company that never fit your strategy in the first place.

Stage 1: strategy and acquisition rationale

Every good deal starts with a reason that isn’t “the company was for sale.” A buyer defines what it’s trying to achieve: entering a new market, acquiring a technology or team, consolidating a fragmented sector, or capturing revenue and cost efficiencies from the combination. This strategic rationale becomes the yardstick every later decision is measured against. If a target doesn’t advance the stated goal, no price makes it a good deal.

In practice, the clearest acquisition strategies specify the profile of an ideal target before anyone goes looking: the size range, the geography, the customer base, the margin structure. A corporate-development team at a strategic acquirer will often maintain a running list of targets that fit the thesis, refreshed quarterly. The discipline here prevents the most expensive mistake in M&A, which is buying something because it’s available rather than because it’s right.

Stage 2: target screening and sourcing (buy-side) versus preparing to sell (sell-side)

Now the two sides of the deal diverge, and it’s worth seeing both. On the buy-side, this stage is target screening: filtering the universe of companies down to a shortlist that fits the strategy, usually with help from an investment bank or the firm’s own corporate-development team. Analysts build screens on financial and operational criteria, then rank candidates by fit and likely availability.

On the sell-side, the same stage looks completely different. A company preparing to sell (or its bankers) assembles the materials and readies the business for scrutiny: cleaning up the financials, organising contracts, and deciding whether to run a broad auction or approach a small number of likely buyers. The sell-side goal is to maximise competitive tension and price; the buy-side goal is to find the right target before a competitor does. Same stage, opposite objectives.

Stage 3: first contact, the NDA, and the teaser and CIM

Once a buyer identifies a target, someone makes the first approach, and the first document to change hands is almost always a non-disclosure agreement (NDA). The NDA is what allows the seller to share confidential financials without the information leaking to competitors or the market. No serious diligence happens before it’s signed. This is the confidentiality gate, and it protects both sides.

After the NDA, the sell-side typically shares two documents. First a teaser: a short, anonymous one-or-two-page summary that describes the business without naming it, designed to gauge buyer interest. Then, for buyers who engage, a confidential information memorandum (CIM): a detailed document covering the company’s operations, financials, market position, and growth story. A common question from people new to deals is what the difference is between a teaser and a CIM. The teaser sparks interest while protecting the seller’s identity; the CIM gives a genuinely interested buyer enough to form a preliminary view and decide whether to submit an indication of interest.

Stage 4: preliminary valuation and the combined-value case

With the CIM in hand, the buyer runs a first-pass valuation. This is where the analyst earns their keep. Standard methods include comparable-company analysis (valuing the target against similar listed peers), precedent-transaction analysis (what buyers paid for comparable companies), and a discounted-cash-flow (DCF) model that projects the target’s future cash flows and discounts them to today’s value. The output isn’t a single number but a defensible range.

For a strategic buyer, valuation also folds in combined-value gains: the extra value created by putting the two businesses together. These come in two forms. Cost savings (eliminating duplicate functions, consolidating facilities) are more reliable and easier to model, while revenue gains (cross-selling, new market access) are seductive but notoriously overestimated. The better approach, in our view, is to price the deal on standalone value plus only the combined-value gains you’d bet your bonus on, treating optimistic revenue projections as upside rather than justification. This is the same discipline that runs through professional corporate finance advisory work, where a valuation has to survive a client’s scrutiny, not just support a desired answer.

The term sheet and letter of intent: the deal’s front bookend

Here’s where the deal gets real. After preliminary valuation, a buyer who wants to proceed puts an offer in writing, and that document (a term sheet or letter of intent) is the front bookend of the entire transaction. It’s the first time both sides commit the key economics to paper. But how much of that document holds you to anything? Understanding what it does, and crucially what parts of it bind you, is one of the most valuable things a dealmaker or seller can learn.

What a term sheet contains: price, structure, consideration

A term sheet sets out the principal commercial terms of the proposed deal in a short, mostly non-binding document. At minimum it covers the price (or a valuation range), the deal structure (share purchase versus asset purchase versus merger), and the form of consideration (cash, stock, or a mix). It typically also flags the key conditions, the expected timeline, and any exclusivity the buyer wants while it does diligence.

The structure choice buried in that document matters more than beginners realise. In a share purchase, the buyer acquires the company’s shares and inherits everything: assets, liabilities, contracts, history. In an asset purchase, the buyer cherry-picks specific assets and leaves unwanted liabilities behind, which is cleaner for the buyer but often triggers more tax and consent issues for the seller, while a merger combines two entities into one under a statutory process. The term sheet is where this fork gets decided, and it shapes every document that follows.

Term sheet vs LOI vs definitive agreement

A frequent source of confusion is how a term sheet, a letter of intent (LOI), and a definitive agreement relate to each other. The short answer is that they sit on a spectrum from summary to binding contract. A term sheet and an LOI are close cousins: both are short, mostly non-binding statements of the deal’s key terms, and in practice the names are often used interchangeably, with an LOI usually framed as a letter from buyer to seller. The definitive agreement is the long-form, fully binding contract that governs the deal.

| Feature | Term sheet | Letter of intent (LOI) | Definitive agreement (SPA/merger agreement) |

|---|---|---|---|

| Length | 1 to 3 pages | 2 to 6 pages | Often 50 to 150+ pages |

| Format | Bulleted term list | Formal letter, buyer to seller | Full legal contract |

| Binding? | Mostly non-binding, with select binding clauses | Mostly non-binding, with select binding clauses | Fully binding |

| Timing | Before diligence | Before diligence | After diligence |

| Purpose | Align on key economics | Signal serious intent, secure exclusivity | Govern the whole transaction |

| What it covers | Price, structure, consideration, exclusivity | Same, plus process and conditions | Reps, warranties, covenants, CPs, indemnities |

Which LOI clauses truly bind: exclusivity, confidentiality, no-hire

This is the part that trips people up, and it’s genuinely important. A term sheet or LOI is described as “non-binding,” but that’s a half-truth. The commercial terms (price, structure) are non-binding placeholders that the parties are free to renegotiate as diligence unfolds. But a handful of specific clauses inside the same document are fully binding, and they carry real legal weight.

Three clauses typically bind even in a “non-binding” LOI. Exclusivity (also called a no-shop) legally stops the seller from talking to other buyers for a set period, usually thirty to ninety days, which is what a buyer buys in exchange for spending money on diligence. Confidentiality carries the NDA’s protection into the LOI, and a no-hire or non-solicit clause stops the buyer from poaching the seller’s employees if the deal falls through.

A common question in legal communities is which LOI clauses are enforceable, and the answer is precisely these: the process and protection clauses bind, while the economic terms don’t until they’re captured in the definitive agreement. The concept isn’t unique to M&A, either. Term sheets also appear in startup fundraising, where the same non-binding-headline, binding-exclusivity structure governs a venture financing round.

| Feature | Term sheet | Letter of intent (LOI) | Definitive agreement (SPA / merger agreement) |

|---|---|---|---|

| Length | 1 to 3 pages | 2 to 6 pages | Often 50 to 150+ pages |

| Format | Bulleted term list | Formal letter, buyer to seller | Full legal contract |

| Binding? | Mostly non-binding, select binding clauses | Mostly non-binding, select binding clauses | Fully binding |

| Timing | Before diligence | Before diligence | After diligence |

| Purpose | Align on key economics | Signal serious intent, secure exclusivity | Govern the whole transaction |

| Covers | Price, structure, consideration, exclusivity | Same, plus process and conditions | Reps, warranties, covenants, CPs, indemnities |

Due diligence: the deal’s core workstream

If the term sheet is the front bookend, due diligence is the engine room. This is the stage where a buyer verifies, line by line, that the company it agreed to buy is the company it’s getting. So why do so many deals live or die here? Because it’s the longest single workstream in most deals, and the one where deals most often collapse, get repriced, or get restructured. For anyone working in transaction services or corporate law, this is where the bulk of the billable hours live.

The six diligence streams: legal, financial, tax, commercial, operational, HR

Diligence isn’t one review; it’s several parallel investigations, each run by specialists. Legal diligence examines corporate records, material contracts, litigation, intellectual property, and regulatory compliance, while financial diligence (often called a quality-of-earnings review) tests whether the reported profits are real and sustainable. Tax diligence hunts for hidden tax exposures, and commercial diligence assesses the market, customers, and competitive position. Operational diligence looks at the supply chain, technology, and systems, and human-resources diligence covers employment terms, key-person risk, and any pension or benefit liabilities.

Here’s what that looks like on a live deal. A financial-diligence team takes the seller’s headline profit figure and strips out one-off gains, adjusts for accounting choices, and rebuilds a “normalised” earnings number that a buyer can trust. If that normalised figure comes in materially below the headline, the price the buyer offered in the term sheet is suddenly negotiable, because the term-sheet price was never binding. This is exactly why the economic terms stay non-binding until diligence is done.

Preliminary versus confirmatory due diligence

Diligence usually happens in two waves, and knowing the difference matters. Preliminary due diligence is the lighter, earlier review a buyer does before or around the term sheet, using the CIM and initial data to decide whether to proceed and at roughly what price. Confirmatory due diligence is the deep, exhaustive review after the term sheet is signed and exclusivity is locked, where the buyer verifies every material assumption before committing to a binding contract.

What experienced practitioners know is that confirmatory diligence is where the leverage quietly shifts. Once a seller has granted exclusivity, they can’t shop the deal, so a buyer who uncovers a genuine problem in confirmatory diligence has room to renegotiate. A common question is what confirmatory due diligence confirms: precisely that the specific representations the seller will make in the definitive agreement are true, which is why it runs right up against the drafting of that agreement.

The data room and a typical six-week diligence timeline

Modern diligence runs through a virtual data room (VDR): a secure online repository where the seller uploads thousands of documents and the buyer’s advisers review them with full audit trails of who saw what. Platforms built for this purpose let the seller control access granularly and track engagement. A common question from people new to deals is what goes in a data room. The short answer: every material contract, financial statement, cap table, employee agreement, IP registration, litigation file, and regulatory licence the buyer’s teams need to verify their assumptions.

| Week | Diligence focus | Typical activity |

|---|---|---|

| Week 1 | Data room opens | Seller uploads documents; buyer teams get access; initial request list issued |

| Weeks 2 to 3 | Deep review | Legal, financial, and tax teams work through documents; Q&A log runs |

| Weeks 3 to 4 | Management sessions | Expert calls, site visits, and management presentations |

| Weeks 4 to 5 | Findings synthesis | Each stream drafts findings; red flags escalated to deal leads |

| Weeks 5 to 6 | Reporting | Diligence reports finalised; findings feed the definitive-agreement negotiation |

Fair warning: six weeks is a clean mid-market benchmark, not a promise. A simple private deal can wrap diligence in two weeks, while a complex cross-border acquisition with multiple regulators can run diligence for three months or more. The timeline flexes with the size and messiness of the target, and a data room full of gaps is itself a red flag.

The definitive agreement: the SPA and its key clauses

Once diligence gives a buyer enough comfort to commit, the deal moves to its most legally intense stage: drafting and negotiating the definitive agreement. For a share deal this is the share purchase agreement (SPA); for a statutory merger it’s the merger agreement. This is the long-form contract that legally binds both parties, and every hard-won diligence finding gets translated into a clause here. So where do deal lawyers earn their fee? Right here, in the clauses that decide who bears which risk.

Reps and warranties, covenants, indemnities

Three families of clauses do most of the heavy lifting. Representations and warranties are statements of fact the seller makes about the business (the accounts are accurate, there’s no undisclosed litigation, the company owns its IP), and if any prove false, the buyer has a claim. Covenants are promises about behaviour, split between things the parties will do before closing (run the business normally, seek approvals) and after. Indemnities are the seller’s promise to compensate the buyer for specific losses, often the ones diligence flagged as risks.

Think of it this way. Diligence surfaces the risks, and the definitive agreement allocates them. If financial diligence found a tax position that might be challenged, the buyer doesn’t just accept the risk: it negotiates a specific indemnity so the seller bears that cost if it materialises. The representations tell the buyer what’s true today; the indemnities decide who pays if something turns out not to be.

Conditions precedent, MAC clause, escrow, earn-out, working-capital adjustment

A cluster of mechanical clauses governs how and when the deal completes. Conditions precedent (CPs) are the boxes that must be ticked before closing can happen, most importantly regulatory approvals, and a material adverse change (MAC) clause lets a buyer walk away if something seriously damaging happens to the target between signing and closing. Escrow holds back part of the purchase price in a third-party account to cover potential post-closing claims, while an earn-out ties part of the price to the target hitting future performance targets, bridging a gap when buyer and seller disagree on value. And a working-capital adjustment trues up the final price based on the actual working capital in the business at closing versus an agreed target.

A question that surfaces often in deal circles is what a MAC clause covers in practice. Modern MAC clauses are drafted narrowly and carve out industry-wide or economy-wide events, so a general recession usually won’t trigger one, but a fire that destroys the target’s only factory might. The earn-out is worth flagging too: it looks like an elegant solution to a valuation gap, but earn-outs generate a disproportionate share of post-deal disputes, because buyer and seller read the performance targets differently once the ink is dry.

Who drafts what, and how the negotiation flows

There’s an unwritten choreography to who holds the pen. Conventionally, the buyer’s counsel prepares the first draft of the SPA, because the buyer wants the strongest protections, and the seller’s counsel then marks it up, pushing back on the breadth of warranties and the size of indemnities. The document ping-pongs between the two sides, often through several rounds, until the risk allocation settles. Drafting the SPA and negotiating its clauses is precisely the kind of high-stakes work that sharp contract-drafting skills are built for, since a single poorly-worded warranty can shift millions of rupees of risk from one party to the other.

Financing and signing: locking the deal and announcing it

With the definitive agreement close to final, two things happen in quick succession: the buyer locks down how it’s paying, and both sides sign. These stages are shorter than diligence or drafting, but they’re where the deal stops being conditional intent and becomes a binding commitment. And what happens if the money isn’t lined up first? Miss the financing piece and even a signed deal can fall apart.

Finalising financing: debt and equity

Unless a buyer is paying entirely from cash on hand, it needs to arrange financing before it can sign with confidence. Acquisition financing usually blends debt (loans from banks or bonds) and equity (the buyer’s own capital or, in a private-equity deal, money from the fund). In a leveraged buyout, debt does most of the work, with the target’s own cash flows expected to service the loans after closing. The financing has to be committed (lenders legally on the hook) before a buyer signs, because signing a deal you can’t fund is a fast route to a lawsuit.

What experienced dealmakers watch for here is the link between financing and the signing-to-closing gap. A buyer often signs with committed financing in place but doesn’t draw the funds until closing, weeks or months later. That timing gap is why financing commitments have to hold firm across the entire period, and why a financing failure can trigger a reverse termination fee, which we’ll come to shortly.

Signing and the deal announcement

Signing is the moment both parties execute the definitive agreement. It’s a genuine milestone: the deal is now legally binding, subject only to the conditions precedent being satisfied. For a private deal, signing might happen quietly in a lawyer’s office. For a public company, signing triggers an immediate obligation to announce the deal to the market, because it’s material information that can move the share price.

Here’s a distinction that confuses a lot of people. Signing does not mean the deal is done. At signing, the parties are contractually committed, but ownership hasn’t transferred, money hasn’t moved, and regulators haven’t yet cleared it. That’s why the very next thing to understand is the gap between signing and closing, which is one of the most important concepts in the entire process.

Signing vs closing: what happens in the gap

If there’s one part of the M&A deal process that separates people who genuinely understand deals from those who’ve only read a summary, it’s this. Signing and closing are two distinct events, often separated by weeks or months, and the gap between them has its own rules, risks, and choreography. Miss this distinction and nothing else about the process quite makes sense.

Why signing and closing are separate events

So why aren’t signing and closing the same moment? Because at signing, the parties have agreed to everything, but several conditions still have to be satisfied before ownership can legally pass. The biggest is regulatory approval: antitrust authorities and sector regulators need time to review the combination, and the law often forbids the parties from completing until they’ve cleared it. Other conditions precedent (third-party consents, shareholder votes, financing draw-down) also take time. Signing captures the agreement; the gap is where the conditions get met; closing is when they’re all done and ownership transfers.

Think of it this way. Signing is the promise, and closing is the performance. Between them sits a period where both sides are legally bound to complete but physically cannot yet, because a regulator hasn’t spoken or a consent hasn’t arrived. It’s a strange limbo: the deal is certain enough to announce, but not yet real.

The 60 to 120 day gap: satisfying conditions and the regulatory standstill

For most mid-to-large deals, the signing-to-closing gap runs roughly sixty to a hundred and twenty days, driven mainly by how long the competition authority takes. During this window, the parties work through the conditions-precedent checklist: filing for and obtaining antitrust clearance, securing sector approvals, collecting change-of-control consents from key customers and lenders, and holding any required shareholder vote. Meanwhile, a standstill applies. Merger-control rules generally forbid the buyer and seller from combining operations (a prohibited “gun-jumping”) until clearance lands, so the target has to keep running as an independent business even though its sale is signed.

The covenants in the definitive agreement govern this period tightly. The seller typically promises to run the business in the ordinary course, not to take major decisions without the buyer’s consent, and to help obtain the approvals. A common question is why the buyer can’t just start integrating the moment the deal is signed. The answer is that antitrust law treats premature coordination between competitors as unlawful, so integration planning can happen, but actual integration has to wait for the clearance that closing depends on.

When deals sign and close simultaneously: simple private deals

Not every deal has a gap. A simple private acquisition (a small, unregulated target with no antitrust concern and no third-party consents needed) can sign and close on the same day, sometimes in the same meeting. This is called a simultaneous sign-and-close, and it’s common at the smaller end of the market. The distinction between the two events only becomes a live issue when a condition precedent (usually a regulatory filing) forces a wait, and the bigger and more regulated the deal, the wider the gap, which is why the largest cross-border transactions can wait a year or more between signing and closing.

Regulatory approvals and closing: the back bookend

We’ve reached the back bookend. Once the definitive agreement is signed, the deal’s fate rests largely in the hands of regulators, and closing can’t happen until they’ve cleared it. So who has to say yes before a deal can close? This stage is where a transaction that made perfect commercial sense can still be blocked, remedied, or delayed by a competition authority. For anyone advising on cross-border deals, understanding which approvals bite, and in which country, is essential.

Antitrust and competition clearance: HSR in the US, CCI in India

The single most important approval in most large deals is merger control: the competition regulator’s sign-off that the combination won’t harm competition. In the United States, deals above certain size thresholds must be notified under the Hart-Scott-Rodino Act, after which a mandatory waiting period runs before the parties can close. In India, the equivalent gatekeeper is the Competition Commission of India (CCI), which reviews “combinations” that cross statutory asset or turnover thresholds under the Competition Act, 2002. Both regimes are suspensory, meaning the parties legally cannot complete until clearance is granted or the waiting period expires.

What experienced practitioners flag here is that antitrust clearance isn’t binary. A regulator can approve unconditionally, approve subject to remedies (requiring the merged company to sell off overlapping assets), or block the deal outright. The possibility of remedies is why the definitive agreement carefully allocates “regulatory risk”: who bears the cost, and how far the buyer must go, if the authority demands divestitures as the price of approval.

Sector and securities approvals: SEBI, RBI/FEMA, shareholder and board votes

Antitrust is rarely the only approval. Depending on the target and the parties, a deal may also need sector-specific clearances (banking, insurance, telecom, and defence are heavily regulated in most countries) and securities approvals. In the US, a merger involving a public company triggers Securities and Exchange Commission (SEC) disclosure and, usually, a shareholder vote via a proxy statement. In India, an acquisition of a listed company can trigger the SEBI Takeover Code, a cross-border deal needs to comply with foreign-exchange rules (both covered in detail in the Indian-law section), and board approval plus, for major deals, shareholder approval sit on the checklist too.

Closing mechanics: CP satisfaction, consideration transfer, ownership passes

Closing is the choreographed final act. Once every condition precedent is satisfied, the parties hold a closing (increasingly a virtual one) where the mechanical steps execute in a set order: final CPs are confirmed as met, the buyer transfers the consideration (wiring the cash or issuing the shares), the seller delivers the share transfers and company records, and legal ownership of the target passes to the buyer. Officers may resign and be replaced, bank mandates change, and the target formally comes under new ownership. The moment all of this completes, the deal is closed: the thing the founder in our opening thought had happened at the term sheet has, finally, happened.

Post-merger integration: where deal value is won or lost

Closing feels like the end, but for the people who have to make the deal pay off, it’s the starting gun. So why do so many well-negotiated deals still disappoint? Post-merger integration (PMI) is the twelfth and final stage, and it’s where the combined-value gains promised in the valuation either materialise or evaporate. A deal can be flawlessly negotiated and still fail here, which is why integration deserves as much attention as any earlier stage, even though it gets a fraction of the glamour.

Day-1 planning and the first 100 days

Serious acquirers don’t wait until closing to think about integration. They build a Day-1 plan during the signing-to-closing gap (the one thing they’re allowed to do while actual integration waits for clearance), covering what must work the moment the deal closes: payroll, IT access, customer communications, and legal entity changes. The “first 100 days” then becomes the intense sprint where the integration team executes the plan, combines systems and teams, and starts capturing the cost and revenue gains the deal was priced on.

A common question is why the first 100 days get singled out. It’s because momentum decays fast: employees and customers form their impressions of the combined company early, key talent decides whether to stay in the first few months, and cost-saving programmes that stall in the opening weeks rarely recover. What experienced integrators know is that a mediocre deal with excellent integration usually beats an excellent deal with poor integration.

Capturing combined value versus integration risk: why most value leaks here

Here’s the second-order effect most people miss. The financial case for an acquisition is built on the promise of combined value (cost savings and revenue gains), but that value is captured (or lost) entirely during integration, long after the deal team that priced it has moved on. Study after study over the decades has found that a large share of acquisitions fail to create the value their models predicted, and integration is where the leakage happens: culture clashes, customer defections, and delayed cost savings quietly erode the returns. The cost overruns and revenue misses that surface here don’t just hurt one deal; they feed back into how acquirers price the next one, making disciplined buyers more conservative on their combined-value assumptions over time. In our view, the honest lesson is that value in M&A isn’t created at signing, it’s created or destroyed in the eighteen months after closing.

Buy-side vs sell-side: the same deal from two seats

Every deal is really two deals happening at once: the one the buyer experiences and the one the seller experiences. So how does the same transaction look from each seat? They share the same stages but pursue opposite goals, and understanding both perspectives makes you far better at either. It also explains a lot of the tension in a negotiation, because what’s a win for one side is often a concession from the other.

The buy-side journey: strategy to screen to diligence to integrate

From the buyer’s seat, the process is about finding the right target and paying no more than it’s worth. The buy-side journey runs: define the acquisition strategy, screen and source targets, approach and sign an NDA, run preliminary then confirmatory diligence, negotiate the definitive agreement to allocate risk in the buyer’s favour, arrange financing, clear regulators, close, and integrate. The buyer’s whole incentive is caution: verify everything, protect against every risk, and avoid overpaying. The people who run this analysis day to day, the analysts who model these deals and stress-test the price, sit squarely on the buy-side when they’re advising an acquirer.

The sell-side journey: prep to CIM/teaser to auction/IOIs to close

From the seller’s seat, the process is about maximising price and certainty of close. The sell-side journey runs: prepare the business for sale, appoint advisers, produce the teaser and CIM, run a process (a broad auction or a targeted approach), collect indications of interest (IOIs) and then binding offers, grant exclusivity to the winning bidder, survive confirmatory diligence, negotiate the definitive agreement to limit the seller’s post-closing exposure, and close. The seller’s incentive is the mirror image of the buyer’s: create competitive tension, disclose enough to satisfy diligence without giving away leverage, and cap the warranties and indemnities that could come back as claims.

Where the two processes converge

For all their opposing goals, the two journeys meet at the same milestones, and seeing them side by side makes the whole process click.

| Stage | Buy-side (acquirer) | Sell-side (target/seller) |

|---|---|---|

| Origination | Define strategy, screen targets | Decide to sell, appoint advisers |

| Marketing | Receive teaser, request CIM | Issue teaser, share CIM |

| Offer | Submit IOI, then term sheet/LOI | Evaluate offers, grant exclusivity |

| Diligence | Run confirmatory diligence | Populate data room, answer Q&A |

| Contract | Draft SPA, push for broad protections | Mark up SPA, cap warranties/indemnities |

| Completion | Fund, clear regulators, close, integrate | Deliver shares, meet CPs, exit |

The M&A deal process under Indian law: CCI, NCLT, SEBI, FEMA

Everything above describes the universal shape of a deal. But what changes when the target sits in Gurugram rather than Delaware? A live Indian transaction runs on top of a specific legal framework, and this is the layer that turns textbook knowledge into practice for anyone working on deals in India. Four regimes govern the process: the Companies Act for mergers, the Competition Act for antitrust, the SEBI Takeover Code for listed-company acquisitions, and FEMA for cross-border money. Get this mapping right and you can run an Indian deal; get it wrong and the transaction can be void.

Governing framework: Companies Act 2013, Competition Act, SEBI Takeover Code 2011, FEMA

The backbone of Indian M&A is a set of four sources. Court-supervised mergers, amalgamations, and schemes of arrangement are governed by Section 230 to 240 of the Companies Act, 2013, which sets out how a scheme is approved and sanctioned, while antitrust review sits under the Competition Act, 2002, administered by the CCI. Acquisitions of listed companies are governed by the SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011, commonly called the Takeover Code. And any cross-border element (a foreign buyer, an overseas seller, funds moving in or out) must comply with the Foreign Exchange Management Act, 1999, administered by the RBI. Most substantial Indian deals touch at least three of these four.

When CCI approval is required: asset/turnover thresholds and the 2024 Deal-Value Threshold

The threshold question in every Indian deal is whether it needs CCI approval. Historically, a transaction qualifies as a notifiable “combination” only if the parties cross specified asset or turnover thresholds set under the Competition Act. That meant a deal below the thresholds escaped merger control entirely, which left a gap: acquisitions of high-value but low-revenue targets (think a large-valuation tech or digital company with modest turnover) could slip through. To close that gap, India introduced a Deal-Value Threshold: transactions with a deal value above ₹2,000 crore, where the target has substantial business operations in India, now require CCI notification regardless of the traditional asset and turnover tests. Enabled by the Competition (Amendment) Act, 2023 and brought into force through the CCI (Combinations) Regulations, 2024 with effect from 10 September 2024, this brought a wave of previously exempt digital-economy deals into the merger-control net.

A common question is when exactly CCI approval becomes mandatory. The practical answer: if a deal crosses either the traditional asset/turnover thresholds or the new Deal-Value Threshold (and no exemption applies), it must be notified to the CCI and cannot close until cleared. Like the US HSR regime, Indian merger control is suspensory, so completing a notifiable combination without approval is “gun-jumping” and exposes the parties to penalties.

The NCLT scheme of arrangement and timeline

When a deal is structured as a formal merger or amalgamation rather than a simple share purchase, it runs through the National Company Law Tribunal (NCLT) as a “scheme of arrangement” under Section 230 to 232 of the Companies Act, 2013. The process has a recognisable rhythm. The companies file a first-motion application; the NCLT may order meetings of shareholders and creditors; the scheme must be approved by the requisite majority (under Section 230(6), a majority in number representing three-fourths, or 75%, in value of each class present and voting); regulators and affected parties get notice; and finally the NCLT hears the second-motion petition and sanctions the scheme. The whole court-supervised process typically takes around six to twelve months, which is why merger structures are slower than straight share acquisitions in India.

Stamp duty on the NCLT sanction order and the appointed date

Two India-specific mechanics catch people out. First, stamp duty: the NCLT order sanctioning a scheme of arrangement is generally chargeable to stamp duty as an instrument of transfer under the Indian Stamp Act, 1899, and because stamp duty is a state subject, the rate varies from state to state. On a large merger, this can be a material cost that structuring often has to account for. Second, the appointed date: a scheme specifies an “appointed date” from which the merger is treated as effective for accounting and tax purposes, which can differ from the “effective date” when the NCLT order is filed with the registrar, and the gap between the two has real accounting and tax consequences that are a classic source of error.

Fast-track mergers under Section 233: what’s changing

Not every Indian merger needs the full NCLT route. Section 233 of the Companies Act, 2013 provides a “fast-track” merger for specified categories, which bypasses the tribunal and is instead approved by the Central Government through the Regional Director. This is faster and cheaper than a full scheme. The section itself covers mergers between two or more small companies and between a holding company and its wholly-owned subsidiary, and it empowers the Central Government to prescribe further eligible classes by rule. That scope has been widened over time. Through amendments to the Companies (Compromises, Arrangements and Amalgamations) Rules notified in September 2025, the Ministry of Corporate Affairs added further categories to the fast-track route, including two or more unlisted companies (other than Section 8 companies) that meet prescribed thresholds of outstanding loans, debentures or deposits with no recent repayment default, and a holding company merging with its subsidiary companies (other than where the transferor is a listed company). This pulls more small and group-internal mergers out of the congested NCLT process and shortens timelines further. For anyone advising smaller companies, the fast-track option is worth checking first, because it can save months.

How long does an M&A deal take? Realistic stage-by-stage timelines

“How long will this take?” is the question every founder, analyst, and junior lawyer asks first, and the honest answer is that it depends enormously on size and regulation. A tiny private deal can close in weeks; a regulated cross-border merger can take well over a year. Setting realistic expectations up front is one of the most useful things an adviser does, because unrealistic timelines are how deals lose momentum and trust.

Simple private deal vs mid-market vs large/regulated

Three broad bands cover most deals. A simple private deal (a small, unregulated target, often a simultaneous sign-and-close) can run from about sixty to ninety days end to end. A mid-market deal (a larger private company with real diligence and perhaps one regulatory filing) typically takes around six months from first approach to close. A large or heavily regulated deal (a public company, multiple antitrust jurisdictions, sector approvals) commonly runs twelve to eighteen months, sometimes longer if a competition authority opens an in-depth review.

| Deal type | Typical timeline | Main driver of duration | Signing-to-closing gap |

|---|---|---|---|

| Simple private deal | ~60 to 90 days | Diligence depth | Often simultaneous |

| Mid-market deal | ~6 months | Diligence + single regulatory filing | ~60 to 90 days |

| Large / regulated deal | ~12 to 18 months | Multi-jurisdiction antitrust + sector approvals | ~4 to 12 months |

| Indian NCLT merger | ~6 to 12 months (court process alone) | NCLT scheme timeline | Runs through the tribunal |

The India-specific timeline

India adds its own timing wrinkle, and it’s worth planning around. Where a deal is structured as an NCLT scheme of arrangement, the court-supervised process alone typically consumes around six to twelve months, on top of any diligence and negotiation that preceded the filing. A straight share acquisition that avoids the NCLT can move faster, but if it triggers CCI approval or the SEBI Takeover Code, those clearances add their own weeks or months. Looking ahead, the widening of the Section 233 fast-track route is the main force likely to compress Indian merger timelines for smaller and group-internal deals, which is a genuine shift worth watching for anyone who works on domestic transactions.

| Stage | Typical duration | Key document | Who leads |

|---|---|---|---|

| Sourcing & NDA | 2 to 6 weeks | NDA, teaser, CIM | Bankers / corporate development |

| Term sheet / LOI | 1 to 3 weeks | Term sheet / LOI | Principals + counsel |

| Due diligence | ~4 to 6 weeks (mid-market) | Diligence reports, VDR | Legal, financial, tax teams |

| Definitive agreement | 2 to 6 weeks | SPA / merger agreement | Deal counsel |

| Signing to closing | ~60 to 120 days | CP checklist, regulatory filings | Counsel + regulators |

| Integration | First 100 days + | Day-1 / integration plan | Integration management office |

Due diligence red flags and common M&A process mistakes

Deals don’t usually die from one dramatic problem. So what kills them? Usually a red flag someone spotted too late, or a process shortcut that seemed reasonable at the time. This closing section is the practitioner’s warning list: the diligence findings that should make a buyer pause, and the process mistakes that quietly wreck otherwise sound deals. Learn these and you’re already ahead of most first-timers.

Financial and legal red flags that surface in diligence

Certain findings should set off alarms. On the financial side: revenue that depends heavily on a single customer, aggressive revenue-recognition that inflates reported profit, a widening gap between reported earnings and actual cash generation, and off-balance-sheet liabilities. On the legal side: undisclosed litigation, weak or unregistered ownership of key intellectual property, change-of-control clauses that let major customers walk when the company is sold, and gaps in regulatory licences. What experienced diligence teams know is that the most dangerous red flag is often not a single finding but a pattern of small evasions, because a seller who’s cagey about the small things is usually hiding something bigger.

Process mistakes: weak term sheet, skipped diligence, no integration plan

The most common process mistakes are self-inflicted. A vague term sheet that leaves key terms “to be agreed” invites painful renegotiation later, and rushed or skipped diligence trades short-term speed for the risk of inheriting an undisclosed liability. Treating integration as an afterthought (no Day-1 plan, no owner for capturing the promised gains) is how a well-priced deal fails to deliver. The mistake we see most often is a buyer so eager to close that it under-invests in diligence, then discovers the problem it should have caught when it’s far more expensive to fix.

How to keep a deal from collapsing between signing and closing

Here’s the second-order lesson that ties the whole process together: a weak term sheet doesn’t just cause problems at the start; it cascades all the way to closing. When early terms are loose, confirmatory diligence becomes the place where the buyer re-opens price, and because the seller has already granted exclusivity, the deal can stall in a bruising renegotiation right before it’s meant to complete. The way to keep a deal alive across the signing-to-closing gap is to front-load the discipline: a precise term sheet, thorough confirmatory diligence, tightly drafted conditions precedent, and interim covenants that keep the business intact. Deals that collapse late almost always trace back to corners cut early, so the fix is boring but reliable: do each stage properly, in order, the first time.

Frequently asked questions

How many stages are there in an M&A deal? Most practitioners describe around twelve stages, grouped into three phases: pre-deal (strategy, sourcing, NDA, valuation), deal execution (term sheet, due diligence, definitive agreement, financing, signing), and completion (regulatory approvals, closing, integration). The exact count varies because some frameworks combine or split stages, but the sequence and logic stay the same across deals.

What is the difference between a term sheet and a letter of intent (LOI)? Very little in substance. Both are short, mostly non-binding documents that set out the key commercial terms before due diligence begins. An LOI is usually framed as a formal letter from the buyer to the seller, while a term sheet is often a bulleted list, but the names are frequently used interchangeably. Both typically contain a few binding clauses, such as exclusivity and confidentiality.

What is a definitive agreement in M&A? The definitive agreement is the long-form, fully binding contract that governs the transaction. For a share deal it’s the share purchase agreement (SPA); for a statutory merger it’s the merger agreement. It contains the representations and warranties, covenants, conditions precedent, indemnities, and price-adjustment mechanics that turn an agreed headline price into an enforceable deal.

How long does M&A due diligence take? For a mid-market deal, confirmatory due diligence typically runs around four to six weeks. A simple private deal can wrap in as little as two weeks, while a large or cross-border target can take three months or more. The timeline depends on the size and complexity of the business and how well-organised the data room is.

How long does the whole M&A process take, from term sheet to closing? It depends on size and regulation. A simple private deal can go from term sheet to closing in about sixty to ninety days, a mid-market deal in roughly six months, and a large or heavily regulated deal in twelve to eighteen months. In India, a merger structured through the NCLT adds around six to twelve months for the court process alone.

What is the difference between signing and closing in M&A? Signing is when both parties execute the definitive agreement and become legally bound. Closing is when ownership transfers and the consideration is paid, which can only happen once every condition precedent (chiefly regulatory approval) is satisfied. The two are often separated by weeks or months; in simple private deals they can happen simultaneously.

What is confirmatory due diligence? Confirmatory due diligence is the deep, detailed review a buyer conducts after signing the term sheet and securing exclusivity, to verify every material assumption before committing to the binding definitive agreement. It confirms that the representations the seller will make in the SPA are true, and it’s where a buyer gains leverage to renegotiate if it uncovers a genuine problem.

Which clauses in an LOI are legally binding? Even in a mostly non-binding LOI, a few clauses typically bind: exclusivity (or no-shop), which stops the seller from talking to other buyers for a set period; confidentiality, which protects shared information; and often a no-hire or non-solicit clause. The commercial terms, such as price and structure, remain non-binding until they’re captured in the definitive agreement.

What is a MAC (material adverse change) clause? A material adverse change clause lets a buyer walk away from a signed deal if something seriously damaging happens to the target between signing and closing. Modern MAC clauses are drafted narrowly and usually carve out industry-wide or economy-wide events, so a general downturn rarely triggers one, but a disaster specific to the target might.

What is a breakup fee (and a reverse termination fee)? A breakup fee is a payment the seller owes the buyer if the seller walks away, for example to accept a higher competing offer. A reverse termination fee is the mirror image: a payment the buyer owes the seller if the buyer fails to complete, often because its financing fell through or it couldn’t obtain regulatory approval. Both are negotiated in the definitive agreement to compensate for a failed deal.

Which laws govern M&A in India? Four main regimes: the Companies Act, 2013 (Section 230 to 240) for court-supervised mergers and schemes of arrangement through the NCLT; the Competition Act, 2002 for CCI merger control; the SEBI (SAST) Takeover Regulations, 2011 for acquisitions of listed companies; and FEMA, 1999 for any cross-border element. Stamp duty law, which is state-specific, also applies to the transfer.

When is CCI approval required for an M&A deal in India? CCI approval is required when a transaction qualifies as a notifiable “combination,” meaning it crosses the asset or turnover thresholds under the Competition Act, 2002, or the newer Deal-Value Threshold of ₹2,000 crore for deals where the target has substantial Indian operations. Indian merger control is suspensory, so a notifiable deal cannot legally close until the CCI clears it.

How long does NCLT approval take for a merger? An NCLT scheme of arrangement typically takes around six to twelve months from the first-motion application to the final sanction order, depending on the tribunal’s workload and whether any objections arise. This is why merger structures are slower than straight share acquisitions in India, and why the fast-track route under Section 233 (which bypasses the NCLT) is attractive for eligible companies.

Is stamp duty payable on a merger in India? Yes. The NCLT order sanctioning a scheme of arrangement is generally chargeable to stamp duty as an instrument of transfer. Because stamp duty is a state subject, the rate varies across states, and on a large merger it can be a material cost that structuring has to account for.

What happens after an M&A deal closes? Post-merger integration begins. The acquirer combines systems, teams, and processes, and works to capture the cost and revenue gains the deal was priced on, usually against a Day-1 plan and an intense first-100-days sprint. Integration is where much of a deal’s value is either realised or lost, which is why disciplined acquirers treat it as seriously as any earlier stage.

References

Official guidance & regulations

- Filing of Combination Notices: asset and turnover thresholds under Section 5 of the Competition Act, 2002. Competition Commission of India.

- FAQs on the Competition Commission of India (Combinations) Regulations, 2024: Deal Value Threshold of ₹2,000 crore and “substantial business operations in India”. Competition Commission of India (in force from 10 September 2024, enabled by the Competition (Amendment) Act, 2023).

- Foreign Exchange Management (Cross Border Merger) Regulations, 2018. Reserve Bank of India (under the Foreign Exchange Management Act, 1999).

- The Indian Stamp Act, 1899. India Code, Government of India (stamp duty is a State subject; rates vary by State).

- The Companies Act, 2013: Section 230 (compromises and arrangements; Section 230(6) approval threshold). India Code, Ministry of Corporate Affairs.

- The Companies Act, 2013: Section 233 (fast-track merger or amalgamation of certain companies). India Code, Ministry of Corporate Affairs.

- SEBI (Substantial Acquisition of Shares and Takeovers) Regulations, 2011: the Takeover Code (25% open-offer trigger). Securities and Exchange Board of India.

- Premerger Notification Program: the Hart-Scott-Rodino (HSR) Act. U.S. Federal Trade Commission.

- Mergers: proxy statements on Schedule 14A and merger disclosure. U.S. Securities and Exchange Commission (Investor.gov).

This article is for educational purposes only and does not constitute professional, financial, legal, or tax advice. Laws, regulatory thresholds, and procedural timelines vary by jurisdiction and change over time; Indian provisions cited here (Companies Act, 2013, Competition Act, 2002, SEBI Takeover Code, FEMA) and their US counterparts are described in general terms. For guidance specific to your transaction or situation, consult a qualified corporate lawyer, tax adviser, or investment banker.

Allow notifications

Allow notifications