Complete 2026 Enrolled Agent Exam syllabus guide: Part-wise domain breakdown, weightage, pass rates, study hours & India exam centres. Start your Enrolled Agent journey today!

Table of Contents

If you’re a commerce graduate or accounting professional in India looking to break into US taxation, the Enrolled Agent (EA) credential offers one of the most accessible pathways to a lucrative international career.

Unlike the CPA which requires 150 credit hours and US-based experience, the EA exam has no educational prerequisites anyone with a Preparer Tax Identification Number (PTIN) can sit for this federally-recognized examination. The credential grants you unlimited representation rights before the IRS, meaning you can represent any taxpayer on any tax matter in all 50 US states a privilege that even many CPAs don’t possess.

What makes this particularly exciting for Indian professionals is the remote work opportunity. US tax firms are actively hiring India-based EAs who can work during US business hours (which conveniently overlap with Indian evening hours) at salaries ranging from ₹6-25 lakhs annually.

The Special Enrollment Examination (SEE), administered by Prometric on behalf of the IRS, is available at testing centers in Bangalore, Hyderabad, and New Delhi making it entirely possible to earn this US credential without leaving India.

In this comprehensive guide, I’ll break down the complete EA exam syllabus across all three parts, explain the domain weightages and question distribution, and provide strategic insights on preparation sequencing.

Whether you’re a B.Com graduate, a CA dropout exploring alternatives, or an experienced accountant looking to add US tax expertise to your skillset, understanding this syllabus structure is your first step toward becoming an Enrolled Agent.

For a broader understanding of the exam’s eligibility and structure, you may also refer to my article on the IRS Enrolled Agent Exam: Eligibility, Structure & Preparation Guide.

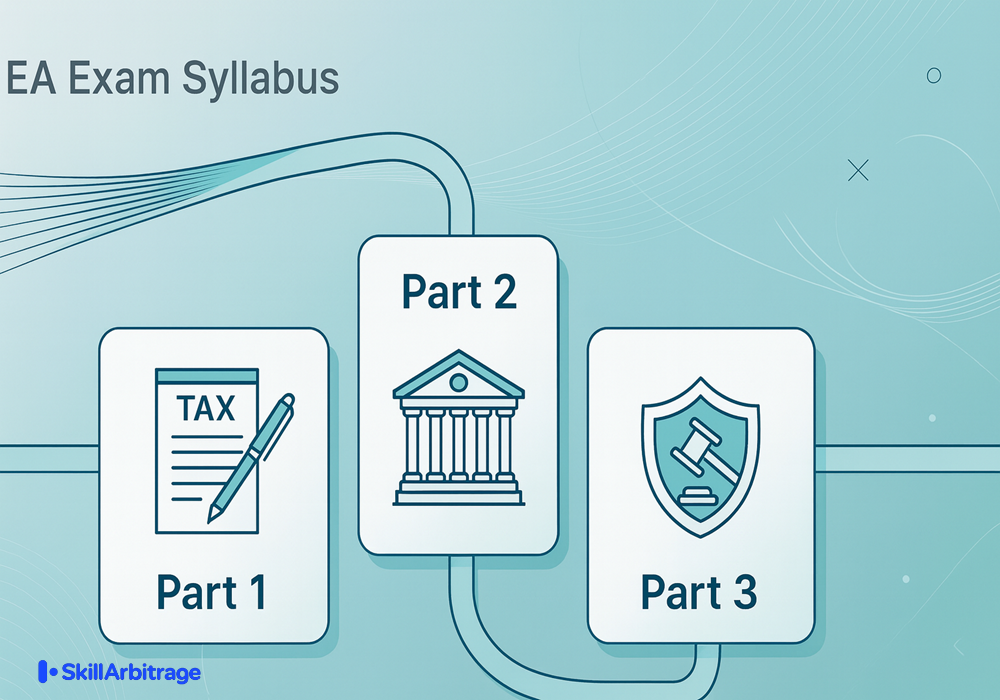

Enrolled agent exam: structure of syllabus

What is the structure of the EA exam syllabus?

Three-part framework: Individuals, Businesses, and Representation

The EA exam is divided into three distinct parts, each testing a specific area of US tax law and IRS procedures. Part 1 focuses on Individual Taxation, covering everything from filing status determination to retirement income and estate taxes. This section is often considered the most intuitive for candidates because much of it relates to personal tax situations that are conceptually similar across countries income, deductions, and credits.

Part 2 shifts to Business Taxation, which many candidates find more challenging due to its complexity around entity types (sole proprietorships, partnerships, C corporations, S corporations), depreciation rules, and specialized business deductions. If you have an accounting background or have studied Indian corporate taxation, you’ll find some concepts familiar, though the specific US rules differ significantly. This part tests your ability to navigate the intricate web of business tax compliance.

Part 3, titled Representation, Practices, and Procedures, is unique because it focuses on the practical aspects of being an Enrolled Agent how to represent clients before the IRS, ethical standards under Treasury Circular 230, audit procedures, appeals processes, and collection matters. Interestingly, this part has the highest pass rate because it builds upon concepts from Parts 1 and 2, and candidates who reach this stage have already developed strong study habits and testing experience.

How domains, weightage, and experimental questions work

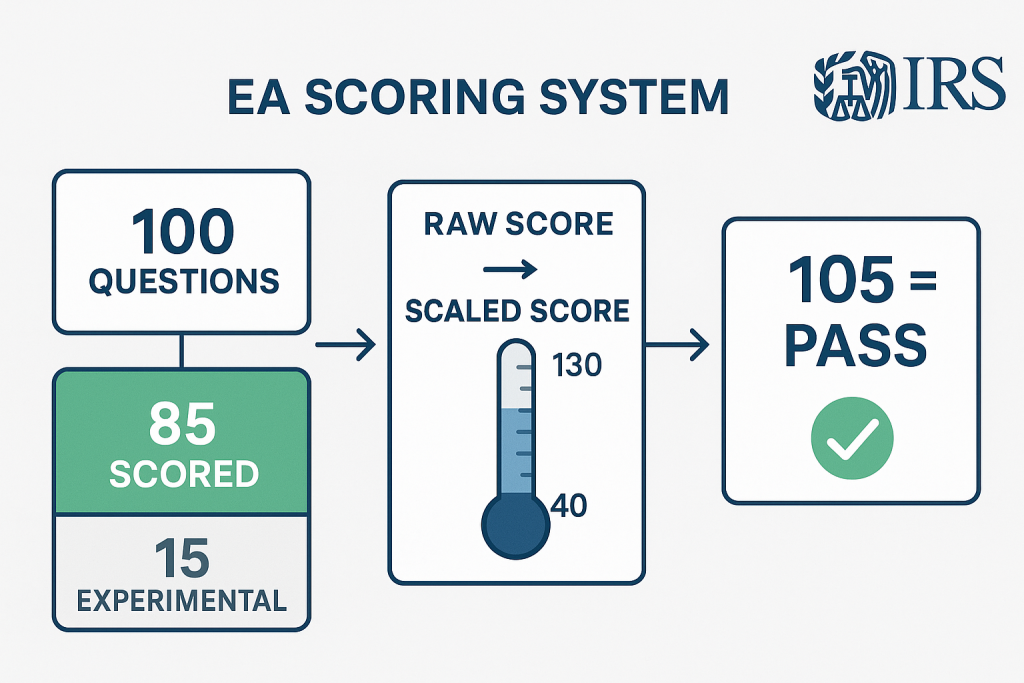

Each part of the EA exam contains exactly 100 multiple-choice questions, but here’s what many candidates don’t realize: only 85 of those questions actually count toward your score. The remaining 15 are experimental questions that the IRS uses to test potential future exam content. These experimental questions are scattered randomly throughout the exam, and you cannot identify which ones they are so you must treat every question as if it counts.

The IRS organizes each exam part into “domains” broad topic areas with specific weightages that determine how many questions you’ll see from each subject. For example, in Part 1, the Income and Assets domain accounts for approximately 20% of scored questions (about 17 questions), while Preliminary Work with Taxpayer Data accounts for 16% (about 14 questions). Understanding these weightages helps you prioritize your study time toward high-yield topics.

The IRS publishes detailed Exam Content Outlines for each part, which break down domains into specific topic lists. These outlines are updated annually to reflect changes in tax law for the May 2025 to February 2026 testing window, the exam tests on tax law as it existed through December 31, 2024. Staying current with these outlines is essential because the IRS regularly adds new topics (like virtual currency taxation and energy credits) while phasing out outdated content.

What is the scoring system and passing criteria?

The EA exam uses a scaled scoring system that ranges from 40 to 130, with 105 being the passing threshold. This scaled approach ensures fairness across different exam versions since the IRS administers multiple versions of the test to maintain security, scaling adjusts for any slight differences in difficulty between versions. Your raw score (the number of questions you answer correctly out of 85 scored questions) is converted to this scale.

What does this mean practically?

You don’t need to aim for perfection. If you can correctly answer approximately 70-75% of the scored questions, you’re likely to pass. However, since you can’t identify which 15 questions are experimental, you should approach every question with equal focus. The IRS doesn’t penalize wrong answers, so never leave a question blank educated guessing is always better than no answer.

When you complete your exam at the Prometric testing center, you’ll receive an immediate pass/fail notification on the screen. If you pass, your score report will simply show “Pass” without revealing your actual score the IRS believes that all passing scores indicate equal qualification. If you fail, you’ll receive a scaled score and diagnostic feedback showing which domains need improvement, which is invaluable for targeted restudying before your retake.

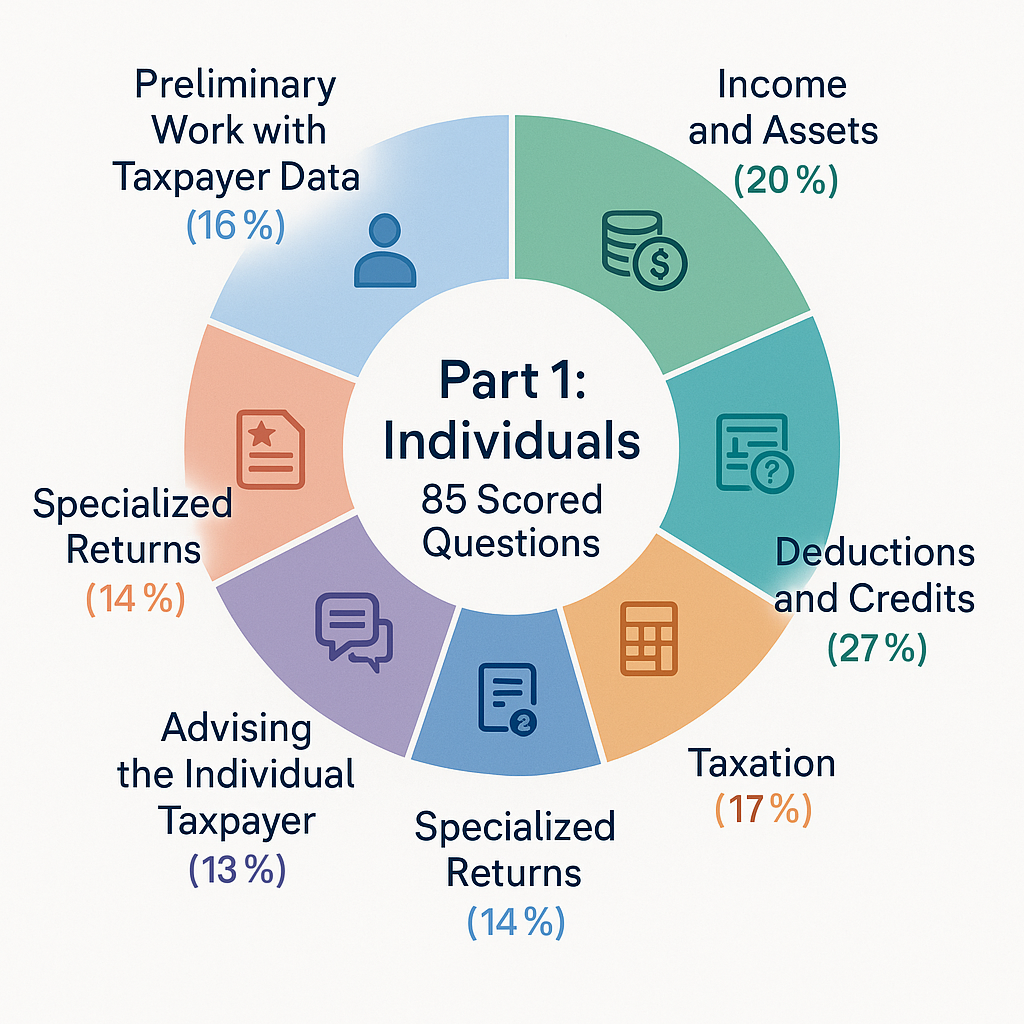

Enrolled agent exam: Part 1 (Individuals)

Domain 1 Preliminary work with taxpayer data

This domain accounts for approximately 16% of Part 1 (about 14 scored questions) and tests your ability to gather and organize taxpayer information before preparing a return. You’ll need to master filing status determination Single, Married Filing Jointly, Married Filing Separately, Head of Household, and Qualifying Surviving Spouse and understand the specific criteria that qualify taxpayers for each status. This includes residency rules, which become particularly relevant for US citizens living abroad or non-resident aliens.

Dependency rules are heavily tested in this domain. You must understand both the Qualifying Child and Qualifying Relative tests, including the support test, relationship test, age test, and joint return test. The IRS frequently asks scenario-based questions where you must determine whether a particular individual qualifies as a dependent and which taxpayer can claim them when multiple people provide support.

The domain also covers PTIN requirements, due diligence obligations for tax preparers, and the proper handling of taxpayer documentation. For Indian professionals, this section introduces you to US-specific concepts like Social Security Numbers, Individual Taxpayer Identification Numbers (ITINs), and the documentation requirements for various deductions and credits. Understanding Form W-2, Form 1099 series, and other information returns is essential.

Domain 2 Income and assets

Domain 2 is the largest in Part 1, accounting for approximately 20% of scored questions (about 17 questions). This section tests your comprehensive knowledge of what constitutes taxable income under US law wages, salaries, tips, interest, dividends, rental income, capital gains, business income reported on Schedule C, and various other income sources. You’ll need to understand the difference between ordinary income and capital gains, and how each is taxed differently.

Retirement income receives significant attention in this domain. You must understand the taxation of distributions from IRAs (Traditional vs. Roth), 401(k) plans, pension plans, and Social Security benefits. The rules around early withdrawal penalties, required minimum distributions, and rollover provisions are frequently tested. Property transactions including the calculation of basis, recognition of gains and losses, and the special rules for personal residence sales are also heavily emphasized.

For 2025, the IRS has added new topics including capital gains and losses on virtual currency transactions and the proper reporting of 1099-NEC and 1099-K income. Adjustments to income such as student loan interest deductions, educator expenses, and IRA contributions are tested here as well. Understanding the flow from gross income to adjusted gross income (AGI) is fundamental to this domain.

Domain 3 Deductions and credits

This domain also accounts for approximately 20% of Part 1 (about 17 questions) and focuses on how taxpayers can reduce their tax liability through deductions and credits. You’ll need to master the choice between standard deduction and itemized deductions, and understand when itemizing makes sense. Itemized deductions include medical expenses (subject to the 7.5% AGI floor), state and local taxes (SALT, capped at $10,000), mortgage interest, charitable contributions, and casualty losses in federally declared disaster areas.

Tax credits receive heavy emphasis because they directly reduce tax liability dollar-for-dollar, unlike deductions which only reduce taxable income. You must understand refundable credits (like the Earned Income Tax Credit and the refundable portion of the Child Tax Credit) versus non-refundable credits (like the Child and Dependent Care Credit and education credits). The eligibility requirements, income phase-outs, and calculation methods for each credit are frequently tested.

The Qualified Business Income (QBI) deduction under Section 199A is a newer addition that allows eligible self-employed individuals and pass-through business owners to deduct up to 20% of their qualified business income. Understanding the limitations based on taxable income, specified service trade or business (SSTB) rules, and W-2 wage limitations is essential. Energy credits and retirement savings contribution credits are also tested in this domain.

Domain 4 Taxation of individuals

Domain 4 covers approximately 17% of Part 1 (about 15 questions) and focuses on the actual calculation of tax liability. You’ll need to understand the progressive tax bracket structure, how to apply tax tables and tax rate schedules, and the calculation of the Alternative Minimum Tax (AMT) for individuals. Self-employment tax the Social Security and Medicare taxes that self-employed individuals must pay is heavily tested, including the calculation of net earnings from self-employment.

Estimated tax payments are important in this domain.

You must understand who is required to make estimated payments, the safe harbor rules to avoid underpayment penalties, and the quarterly due dates. The rules around household employment taxes (the “nanny tax”) and the taxation of tip income are also covered. Understanding how to calculate total tax liability, apply withholding and credits, and determine whether a taxpayer owes or is due a refund is fundamental.

Net Investment Income Tax (NIIT) the additional 3.8% tax on investment income for high earners is tested here as well. You’ll need to understand the income thresholds that trigger this tax and which types of income are subject to it. The domain also covers tax provisions for members of the military and the implications of filing joint returns versus separate returns on overall tax liability.

Domain 5 Advising the individual taxpayer

This domain accounts for approximately 13% of Part 1 (about 11 questions) and tests your ability to provide strategic tax advice to individual clients. You’ll encounter questions about estimated tax planning, including mid-year adjustments to withholding or estimated payments based on changing income circumstances. The timing of income recognition and deduction acceleration strategies for year-end tax planning are frequently tested.

Joint and several liability on married filing jointly returns is an important concept both spouses are fully liable for the entire tax due, even if only one earned the income.

You’ll need to understand innocent spouse relief, separation of liability relief, and equitable relief provisions that can protect one spouse from the other’s tax liabilities. Injured spouse claims, which protect a spouse’s refund from being applied to the other spouse’s prior obligations, are also tested.

The domain covers conditions for filing claims for refund, statute of limitations on assessments and collections, and penalties for perjury and frivolous positions. Understanding when and how to amend returns, the consequences of understating income or overstating deductions, and the preparer’s due diligence requirements helps you advise clients responsibly while protecting yourself from penalties.

Domain 6 Specialized returns (Estate, Gift, International)

Domain 6 covers approximately 14% of Part 1 (about 12 questions) and addresses less common but important individual tax situations.

Estate tax and Form 706 filing requirements are tested you’ll need to understand the applicable exclusion amount, portability of the deceased spouse’s unused exclusion, and the types of property included in a gross estate. While most estates don’t owe federal estate tax due to the high exemption, understanding the filing requirements and deadlines is essential.

Gift tax provisions and Form 709 requirements are frequently tested. You must understand the annual exclusion amount, the lifetime gift tax exemption (which is unified with the estate tax exemption), and which transfers constitute taxable gifts. The rules around gifts to spouses, educational and medical exclusions, and gift-splitting between married couples are important concepts.

International information reporting requirements round out this domain. Form 1116 for foreign tax credits, FBAR (FinCEN 114) for foreign bank account reporting, and FATCA requirements are increasingly tested as the IRS focuses on international compliance. For Indian professionals advising US taxpayers with foreign connections or US citizens living abroad these topics are particularly relevant to your future practice.

Part 2 (Businesses) of enrolled agent exam

Domain 1 Business entities and tax considerations

Domain 1 is the largest in Part 2, accounting for approximately 35% of scored questions (about 30 questions). This domain tests your understanding of different business entity types and their tax implications a foundational knowledge area that determines how virtually all business tax questions are approached.

You’ll need to master the characteristics, formation requirements, and tax treatment of sole proprietorships, partnerships, limited liability companies (LLCs), C corporations, and S corporations.

Sole proprietorships are the simplest entity type, with business income reported directly on the owner’s Schedule C. Partnerships and multi-member LLCs file Form 1065 as information returns, with income, deductions, and credits flowing through to partners on Schedule K-1. You must understand the allocation of partnership items, the treatment of guaranteed payments to partners, and the basis rules that determine the tax consequences of distributions and losses.

C corporations are taxed as separate entities under Subchapter C, filing Form 1120 and paying corporate income tax on their profits. When profits are distributed as dividends, shareholders pay tax again the “double taxation” phenomenon. S corporations, which file Form 1120-S, elect pass-through treatment under Subchapter S, avoiding double taxation but subject to strict eligibility requirements, including the 100-shareholder limit and single class of stock rule.

The domain heavily tests entity formation and selection considerations when to recommend each entity type based on liability protection, self-employment tax implications, fringe benefit availability, and exit strategies. You’ll encounter questions about the tax consequences of contributing property to entities, the requirements for making S elections, and the circumstances that can cause inadvertent termination of S corporation status.

Domain 2 Business income, deductions, depreciation & asset rules

Domain 2 accounts for approximately 44% of Part 2 (about 37 questions), making it the most heavily weighted domain. This section tests your comprehensive knowledge of business income recognition, deductible expenses, and the complex rules surrounding business assets.

You’ll need to understand the difference between cash and accrual accounting methods, the rules for changing accounting methods, and the tax treatment of various income sources including sales, services, and passive income.

Business deductions are extensively tested, including ordinary and necessary expense requirements, the distinction between deductible repairs and capital improvements, and the rules around specific expense categories. Vehicle expenses under the actual expense method versus standard mileage rate, home office deductions under the simplified and regular methods, and business meals deductions (currently 50% deductible) are frequently examined. Start-up and organizational costs, which must be capitalized and amortized, receive significant attention.

Depreciation rules form a major component of this domain. You must master the Modified Accelerated Cost Recovery System (MACRS), including recovery periods for different property classes, depreciation conventions (half-year, mid-quarter, mid-month), and the calculation of annual depreciation deductions. Section 179 expensing, which allows immediate deduction of qualifying property costs up to annual limits, and bonus depreciation under Section 168(k) are heavily tested.

The domain also covers asset disposition rules, including the calculation of gain or loss on sale, Section 1231 property treatment, depreciation recapture under Sections 1245 and 1250, and like-kind exchanges under Section 1031. Understanding the relationship between the balance sheet and income statement, analyzing financial records for tax implications, and advising business taxpayers on tax-efficient decisions are all tested concepts.

Domain 3 Specialized returns (trusts, estates, exempt orgs, farmers)

Domain 3 covers approximately 21% of Part 2 (about 18 questions) and addresses specialized business tax situations that require unique knowledge. Trust and estate income taxation is heavily emphasized you’ll need to understand the difference between simple and complex trusts, the distributable net income (DNI) concept that determines the character and amount of distributions taxable to beneficiaries, and the Form 1041 filing requirements.

Exempt organizations under Section 501(c)(3) and related provisions are tested, including the requirements for tax-exempt status, the unrelated business taxable income (UBTI) rules that can subject even exempt organizations to tax, and the annual information return requirements on Form 990. Understanding the private foundation rules, public charity status tests, and the consequences of excess benefit transactions is important.

Retirement plan taxation from the business perspective is covered here the types of qualified plans (defined benefit, defined contribution, 401(k), SEP-IRA, SIMPLE-IRA), contribution limits, nondiscrimination testing, and the tax benefits available to employers who establish plans. Farmer taxation under Schedule F, including special provisions for crop insurance proceeds, commodity credit loans, and farm income averaging, represents the final specialized area in this domain.

What does part 3 (Representation) cover in the enrolled agent exam?

Domain 1 Practices & procedures (including circular 230)

Domain 1 accounts for approximately 30% of Part 3 (about 26 questions) and focuses on the rules governing practice before the IRS. Treasury Department Circular 230 is the foundational document that establishes the standards of conduct for all practitioners attorneys, CPAs, enrolled agents, and others authorized to represent taxpayers. You must understand who may practice before the IRS, the limited practice rights of unenrolled preparers, and the expanded rights granted to enrolled agents.

The requirements for becoming and maintaining status as an Enrolled Agent are tested, including the 72-hour continuing education requirement over each three-year enrollment cycle (with a minimum of 16 hours annually, including 2 hours of ethics). Sanctionable acts that can result in censure, suspension, or disbarment from practice are heavily emphasized these include incompetence, disreputable conduct, giving false opinions, and conflicts of interest.

The rules governing advertising and solicitation, fee arrangements (contingent fees are generally prohibited in tax matters), and the duties owed to clients and the IRS are tested. You’ll encounter questions about the due diligence requirements when relying on client information, the duty to advise clients of errors discovered in prior returns, and the standards for providing written advice. Understanding when you must return client records and the rules about conflicts of interest in representation is essential.

This domain for 2025 has added new emphasis on incompetence as a specifically sanctionable act and conflicts of interest in representation scenarios. The practitioner’s obligations when representing a decedent’s estate and the ethical implications of various representation strategies are increasingly tested.

Domain 2 Representation before the IRS

Domain 2 covers approximately 29% of Part 3 (about 25 questions) and addresses the practical aspects of representing taxpayers in IRS matters. Power of Attorney and Form 2848 are fundamental you must understand how to properly complete this form, the scope of authority it grants, the difference between representation authority and tax information authorization (Form 8821), and when CAF numbers are required.

Building the taxpayer’s case involves gathering and organizing supporting documentation, understanding the types of records that substantiate various deductions and credits, and knowing how long records must be retained. The domain tests your ability to analyze a taxpayer’s financial situation, including the preparation of financial statements for collection matters using Form 433-A (for individuals) and Form 433-B (for businesses).

Legal authority and references are important you must know how to use the Internal Revenue Code, Treasury Regulations, Revenue Rulings, Revenue Procedures, and court cases to support positions. The domain covers the taxpayer’s burden of proof in various proceedings, the effect of amended returns on the statute of limitations, and related procedural issues. For 2025, there’s increased emphasis on the taxpayer’s burden of proof in audit and collection situations.

Domain 3 Audits, appeals & collections

Domain 3 accounts for approximately 23% of Part 3 (about 20 questions) and tests your knowledge of the IRS examination, appeals, and collection processes. The audit process is covered from initial contact through resolution correspondence audits, office audits, and field audits each have different procedures and representation strategies. You must understand taxpayer rights during examination, including the right to representation and the right to request an audit reconsideration.

The IRS Appeals process provides an independent review of disputed issues before litigation. You’ll need to understand when and how to request Appeals consideration, the protest requirements, and the procedures for Alternative Dispute Resolution (ADR) programs like Fast Track Settlement. The 30-day and 90-day letter procedures, the role of the Tax Court in deficiency cases, and the distinction between prepayment and post-payment litigation forums are tested.

Collection procedures receive significant attention from initial notices through enforced collection actions like levies and liens. You must understand the Collection Due Process (CDP) hearing rights, the differences between a levy and a lien, installment agreement options, currently-not-collectible status, and Offers in Compromise. The statute of limitations on collection (generally 10 years from assessment) and the circumstances that can extend or suspend it are frequently tested.

Domain 4 Filing accuracy, documentation & recordkeeping

Domain 4 covers approximately 16% of Part 3 (about 14 questions) and addresses the accuracy, documentation, and recordkeeping requirements for tax practitioners. The accuracy-related penalties negligence penalty, substantial understatement penalty, and fraud penalty are tested along with the reasonable cause exception that can abate these penalties. You must understand the due diligence requirements for claiming credits like the Earned Income Tax Credit and Child Tax Credit.

Record maintenance requirements for both taxpayers and practitioners are covered. Practitioners must retain copies of returns or maintain lists of returns prepared, keep records of continuing education, and maintain required documentation for at least three years. Recognizing duplicate entries and common errors in financial records is tested, as is the ability to identify red flags that suggest inaccurate or fraudulent information.

Electronic filing requirements and procedures are increasingly emphasized, including the rules for authorized e-file providers, the signature requirements for electronic returns, and the acknowledgment and rejection procedures. The consequences of e-file fraud, identity theft procedures, and the practitioner’s role in protecting taxpayer information under Section 7216 round out this domain.

If you want a step-by-step walkthrough of all three exam parts, you can explore the Full Guide on IRS Enrolled Agent Exam, which expands on these components with practical study insights.

Which part of enrolled agent exam part is the hardest?

Why part 2 is considered the most challenging?

Part 2 consistently has the lowest historical pass rates, though recent years have shown improvement (67% in 2023-2024 compared to 57% in 2015-2016). The primary challenge lies in the complexity of business taxation itself you’re essentially learning multiple tax systems simultaneously.

Each entity type (sole proprietorship, partnership, C corporation, S corporation) has its own rules for income recognition, deductions, basis calculation, and distributions. The interplay between these systems creates layered complexity.

The accounting knowledge requirement distinguishes Part 2 from the other sections. While you don’t need to be a CPA, you must understand basic financial statement concepts, the relationship between book and tax income, and how to analyze financial records for tax implications.

For candidates without an accounting background, the depreciation calculations, basis adjustments, and partnership allocation rules can feel overwhelming initially but with dedicated study, these concepts become manageable.

Why part 3 has the highest pass rate?

Part 3 consistently achieves pass rates around 70-75%, making it the “easiest” part statistically. However, this doesn’t mean Part 3 is simple rather, it reflects several structural advantages.

First, most candidates take Part 3 last, meaning they’ve already developed effective study habits and testing strategies from passing Parts 1 and 2. They’re experienced test-takers who understand the exam format and pacing.

Second, Part 3 content builds upon concepts tested in Parts 1 and 2.

When you study representation in audits, you’re applying knowledge about individual and business taxation you’ve already mastered. The procedural nature of Part 3 learning processes, timelines, and rules tends to be more straightforward than the calculation-heavy content of Parts 1 and 2. Many candidates find that dedicated memorization of Circular 230 provisions and IRS procedures yields reliable results.

What causes most candidates to fail part 1?

Part 1 pass rates have declined in recent years, dropping to 56% in 2023-2024. The primary cause appears to be underestimation because Part 1 covers “individual” taxation, many candidates assume it’s straightforward based on personal tax experience. They allocate insufficient study time, particularly for specialized topics like estate and gift taxation, international reporting, and the numerous credits with varying eligibility requirements.

The breadth of coverage in Part 1 is deceptive. While each topic may seem simple in isolation, the exam tests nuanced scenarios that require deep understanding. Questions often present complex family situations requiring dependency determinations, capital gain calculations with basis adjustments, or retirement account scenarios involving early withdrawals and rollovers. Candidates who surface-study each topic without practicing application through multiple-choice questions often struggle on exam day.

What order should I take the enrolled agent exam in?

Best exam sequence for commerce and non-accounting backgrounds

For commerce graduates and professionals without extensive US accounting experience, I recommend starting with Part 1 (Individuals).

The concepts of personal income, deductions, and credits are more intuitive and relatable to your own tax experiences, even if those experiences are with Indian taxation. This allows you to build confidence with the exam format and study process while learning foundational US tax concepts that will support your understanding of Parts 2 and 3.

After passing Part 1, take Part 3 (Representation) next.

This sequence might seem counterintuitive since Part 2 (Businesses) is often considered the natural progression. However, Part 3’s procedural content reinforces individual tax concepts while introducing you to the professional practice of an Enrolled Agent. By the time you tackle Part 2, you’ll have two parts under your belt, established study routines, and the confidence to face the most challenging material.

When should you attempt part 2 based on accounting comfort?

If you have a strong accounting background perhaps you’ve completed CA Intermediate, have bookkeeping experience, or work in corporate finance you might consider taking Part 2 earlier in your sequence.

Your familiarity with depreciation, entity structures, and financial statement analysis gives you a head start on the most calculation-intensive content. Some accounting professionals even start with Part 2 to tackle the hardest material while their technical knowledge is fresh.

However, even with accounting experience, don’t underestimate the US-specific rules that differ from Indian GAAP or Ind-AS.

The MACRS depreciation system, S corporation eligibility requirements, and partnership basis calculations have no direct Indian equivalents. Allocate sufficient study time regardless of your background, and supplement your accounting knowledge with targeted study of US-specific provisions. Most experts recommend a minimum of 80-100 study hours for Part 2 regardless of your starting point.

Recommended study hours for each part of enrolled agent exam

The consensus among EA review course providers and successful candidates is that you should allocate approximately 80-100 hours of study time for Part 1 and Part 2 each, and 60-80 hours for Part 3. This translates to roughly 6-10 weeks per part if you’re studying 10-15 hours weekly a realistic pace for working professionals balancing study with employment and personal commitments.

These estimates assume you’re using a structured EA review course (such as Gleim, Surgent, or Becker) that provides organized study materials, video lectures, and practice questions. Self-study using only IRS publications and free resources typically requires more time because you’ll spend additional hours organizing material and identifying what’s testable. Regardless of your study method, practice questions are essential aim to answer at least 1,000 practice questions per part to build the pattern recognition and pacing skills necessary for exam day success.

How to take the enrolled agent exam in India?

Where can you take the enrolled agent exam in India?

Prometric testing locations: Bangalore, Hyderabad, and New Delhi

The IRS offers international testing for the Special Enrollment Examination at Prometric testing centers in three Indian cities: Bangalore, Hyderabad, and New Delhi. These are the same professional testing facilities used for other international exams like GMAT and GRE, ensuring a standardized, secure testing environment. The centers are equipped with computer workstations, provide scratch paper and calculators, and have proctors who enforce strict testing protocols.

When selecting your testing location, consider factors beyond just proximity.

Bangalore’s Prometric center, for example, is located in a business district with good transport connectivity. Check availability early because international testing dates are more limited than US domestic dates, and popular time slots fill quickly during peak tax season preparation periods. You can view available dates and times through your Prometric account once you’re ready to schedule.

International testing dates and availability

International testing availability typically runs from late June through February of the following year, slightly more restricted than the US domestic testing window of May 1 to February 28.

For the 2025-2026 testing cycle, international testing at Indian centers is available from June 28, 2025, through February 28, 2026. The March-April blackout period applies globally while the IRS updates exam content for the new tax year.

Seat availability varies by location and time of year. The months immediately following the testing window opening (June-July) and the final weeks before the window closes (January-February) tend to be busiest.

Planning your exam dates 2-3 months in advance gives you flexibility in scheduling and adequate time to complete your preparation. Remember that you can take the three exam parts in any order and on different dates you don’t need to complete all three in a single trip to the testing center.

How to schedule your EA exam from India

Creating your Prometric account and scheduling process

Before scheduling your exam, you must first obtain a Preparer Tax Identification Number (PTIN) from the IRS this is required even if you’ve never prepared a US tax return. The PTIN application is completed online through the IRS website and requires basic identifying information; as a non-US resident, you’ll need to provide passport information rather than a Social Security Number. Once you have your PTIN, you’re eligible to schedule your SEE examination.

Create an account at Prometric’s website specifically for IRS examinations.

The scheduling process involves selecting your exam part (SEE Part 1, 2, or 3), choosing your preferred testing location and date, and completing payment. You’ll receive a confirmation email with your appointment details and confirmation number save this information carefully, as you’ll need the confirmation number for any changes and must present it at the testing center.

Exam fee payment and rescheduling policies

The current examination fee is $267 per part (increased from $206 in March 2025), payable at the time of scheduling via credit card (Visa, MasterCard, American Express) or electronic check. The fee is non-refundable and non-transferable, so schedule only when you’re confident in your preparation. Indian candidates should note that this USD payment will be subject to your bank’s foreign transaction fees and the prevailing exchange rate.

Rescheduling policies are strict: you can reschedule at no additional cost if done at least 30 days before your appointment. Rescheduling 5-29 days before costs $35. If you reschedule within 5 days or miss your appointment entirely, you forfeit the full $267 fee and must pay again to reschedule. Given these stakes, build buffer time into your preparation schedule and only book your exam date once you’re consistently scoring 75%+ on practice tests.

For a complete step-by-step pathway tailored for Indian candidates, you can read How to Become a US Enrolled Agent From India, which explains the full process from PTIN to licensing.

Conclusion

The Enrolled Agent exam represents a structured pathway to a valuable credential one that’s particularly accessible for Indian professionals seeking international career opportunities in US taxation. With three parts covering individual taxation, business taxation, and representation practices, the SEE exam tests comprehensive knowledge while remaining achievable with dedicated preparation. The domain-based structure with published weightages allows you to strategically allocate your study time toward high-yield topics.

Your journey begins with obtaining a PTIN, selecting a quality review course, and committing to the approximately 220-280 total study hours needed across all three parts. With testing centers available in Bangalore, Hyderabad, and New Delhi, you can earn this US federal credential without leaving India opening doors to remote work opportunities with US tax firms, freelance consulting engagements, and a career path that transcends geographic boundaries. The investment of time and the $801 total examination fee (plus review course costs) pays dividends through enhanced earning potential and professional recognition that few other credentials can match.

For more information visit our iPleaders blog on Enrolled Agent Exam Syllabus.

Frequently Asked Questions

What are the three parts of the Enrolled Agent exam syllabus?

The EA exam has three parts: Part 1 (Individuals) covers personal taxation including income, deductions, and credits; Part 2 (Businesses) covers entity taxation, depreciation, and specialized returns; Part 3 (Representation) covers IRS practices, Circular 230 ethics, and taxpayer representation.

How many questions are on each part of the EA exam?

Each part contains exactly 100 multiple-choice questions, with 85 questions scored and 15 experimental questions used for future exam development. You have 3.5 hours (210 minutes) to complete each part.

What is the passing score for the Enrolled Agent exam?

The passing score is 105 on a scaled score ranging from 40 to 130. This translates to correctly answering approximately 70-75% of the scored questions, though the exact number varies based on question difficulty.

Can I take the EA exam parts in any order?

Yes, you can take Parts 1, 2, and 3 in any sequence you prefer. Most candidates start with Part 1 (Individuals) and take Part 3 (Representation) last because its content builds on earlier parts.

How long do I have to pass all three parts?

You have three years from the date you pass your first part to pass the remaining parts. If you don’t complete all three within this window, your earliest passed part expires and must be retaken.

What is the EA exam fee for 2025-2026?

The current fee is $267 per part (increased from $206 in March 2025), totaling $801 for all three parts. Additionally, there’s a $140 enrollment fee payable to the IRS after passing all parts.

Which EA exam part is the most difficult?

Part 2 (Businesses) is generally considered most challenging due to complex entity taxation rules and accounting concepts. However, Part 1 has the lowest recent pass rates (56%) due to candidate underestimation.

How many study hours are needed for each EA exam part?

Plan for 80-100 hours each for Parts 1 and 2, and 60-80 hours for Part 3 totaling approximately 220-280 hours. At 10-15 hours weekly, this represents 6-9 months of preparation.

Can I take the Enrolled Agent exam from India?

Yes, Prometric testing centers in Bangalore, Hyderabad, and New Delhi offer the EA exam. International testing for 2025-2026 runs from June 28, 2025, through February 28, 2026.

What topics are most heavily tested on Part 1?

Income and Assets (20%, 17 questions) and Deductions and Credits (20%, 17 questions) are the most heavily weighted domains. Within these, retirement income, capital gains, and refundable credits receive significant emphasis.

Do I need an accounting degree to pass Part 2?

No degree is required, though basic accounting knowledge helps with depreciation, basis calculations, and financial statement analysis. Non-accountants can succeed with additional study time focused on these technical areas.

What is Circular 230 and why does it matter for Part 3?

Treasury Circular 230 establishes ethical standards for practitioners before the IRS, covering conduct rules, advertising restrictions, and sanctionable acts. It’s fundamental to Part 3 and your future practice as an EA.

How often does the EA exam syllabus change?

The IRS updates the exam annually during the March-April blackout period to reflect tax law changes. For May 2025-February 2026 testing, the exam covers tax law through December 31, 2024.

Are there experimental questions on the EA exam?

Yes, 15 of the 100 questions on each part are experimental and don’t count toward your score. They’re indistinguishable from scored questions, so treat every question as if it counts.

What study materials should I use for the EA exam syllabus?

Use a comprehensive EA review course (Gleim, Surgent, or Becker are popular choices) that includes study guides, video lectures, and extensive practice questions. Supplement with IRS publications and the official Exam Content Outlines.

Allow notifications

Allow notifications